Albertsons Companies Inc Fundamental Analysis

Disclaimer: This article by The Globetrotting Investor is general in nature. We aim to bring you long-term focused analysis driven by fundamental data, hence, providing you commentary based on historical data and analyst forecasts only using an unbiased methodology. This is not a buy/ sell recommendation, and it is solely for educational purposes. Please do your research before investing. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Please read the full disclaimer here.

Albertsons Companies Inc

Last Updated: 21 Sep 2022

NYSE: ACI

GICS Sector: Consumer Defensive

Sub-Industry: Grocery Stores

Share this fundamental analysis

Table of Contents

Management

CEO: Vivek Sankaran

Tenure: 3.4 years

Albertsons Companies, Inc.'s management team has an average tenure of 3.7 years. It is considered experienced.

Source of Revenue

Albertsons Companies Inc., through its subsidiaries, engages in the operation of food and drug stores in the United States.

The company and its subsidiaries offer grocery products, general merchandise, health and beauty care products, pharmacy, fuel and other items and services in its stores or through digital channels. It also manufactures and processes food products for sale in stores.

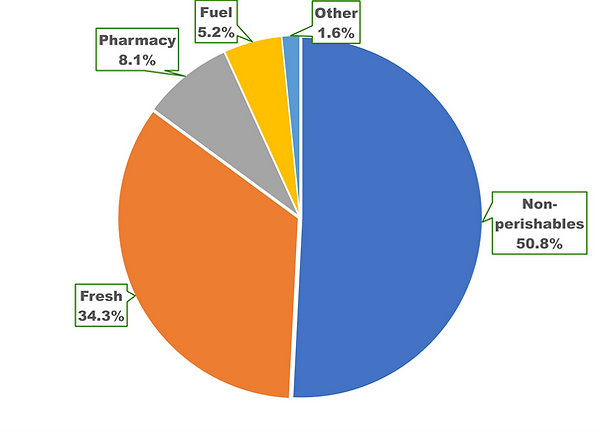

The company has one reportable segment. Instead, it presents its revenue by product type. There are 5 product types:

-

Non-perishables – consists primarily of general merchandise, grocery, dairy and frozen foods. This product generated the highest revenue in fiscal 2021.

-

Fresh – consists primarily of produce, meat, deli, floral and seafood.

-

Pharmacy

-

Fuel

-

Other – consists primarily of wholesale revenue to third parties, commissions, and other miscellaneous revenue.

Digital-related sales are included in the above categories.

As of February 26, 2022, Albertsons Companies Inc. operated 2,276 stores across 34 states and the District of Columbia under 24 banners including Albertsons, Safeway, Vons, Pavilions, Randalls, Tom Thumb, Carrs, Jewel-Osco, Acme, Shaw's, Star Market, United Supermarkets, Market Street, Haggen, Kings Food Markets and Balducci's Food Lovers Market.

Additionally, the company also operated 1,722 pharmacies, 1,317 in-store branded coffee shops, 402 adjacent fuel centres, 22 dedicated distribution centres, 20 manufacturing facilities and various digital platforms.

Albertsons Companies Inc Product Revenue FY2022

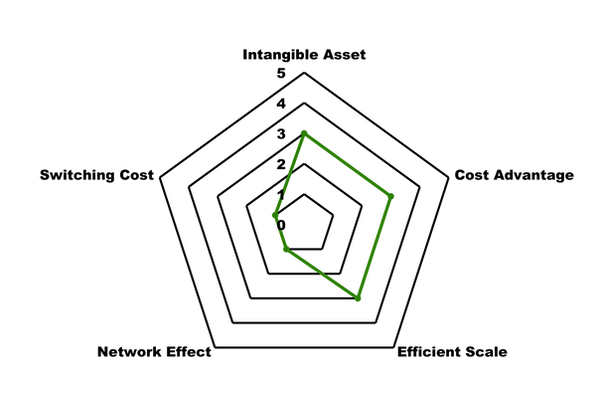

Albertsons Companies Inc Economic Moat

Albertsons Companies Inc Economic Moat

Economic Moat: None

There are many ways to identify Albertsons Companies Inc’s economic moat, but I focus on the above 5 types. The rating is purely subjective and based on my in-depth understanding and analysis of Albertsons Companies Inc. Please check my summary to understand more about the economic moat.

Performance Checklist

Is Albertsons Companies Inc’s revenue growing YoY for the past 5 years consistently? Yes

Is the net income growing YoY for the past 5 years consistently? Yes

Is the cash flow from operating activities growing YoY for the past 5 years consistently? Yes

Is the free cash flow positive for the past 5 years? No

Is the gross margin % consistent/ growing for the past 5 years? Yes

Is the EPS growing for the past 5 years? Yes

Albertsons Companies Inc Revenue, Net Income, Operating Cash Flow, and FCF (USD Million)

Is the free cash flow per share growing for the past 5 years? The general trend shows that it is increasing but it is not conclusive to me.

Albertsons Companies Inc FCF per Share

Management Effectiveness

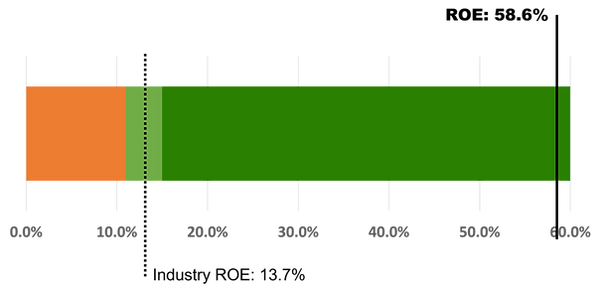

Is Albertsons Companies Inc’s ROE consistently at 12%-15% YoY for the past 5 years? No

Albertsons Companies Inc Return on Equity

Is the ROIC consistently at 12%-15% YoY for the past 5 years? No.

Albertsons Companies Inc Return on Invested Capital vs Weighted Average Cost of Capital

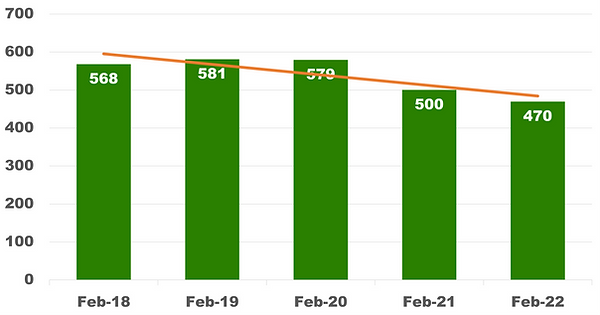

The trendline for the number of shares outstanding is declining, which is something that an investor would be pleased to see.

Albertsons Companies Inc Shares Outstanding (Million Shares)

Albertsons Companies Inc Financial Health

Albertsons Companies Inc Financial Health (USD Million)

Current Ratio: 1.1 (pass my requirement of >1.0)

Debt-to-EBITA: 3.46 (fail my requirement of <3.0)

Interest Coverage: 5.4 (pass my requirement of >3.0) – however, I would pay attention to their interest coverage as it is close to the requirement of 3.0.

Debt Servicing Ratio: 12.98% (pass my requirement of <30.0%)

Dividend

Current Dividend yield: 1.78%

Have the dividend payments been stable for the past 5 years? Not conclusive as the company has been paying dividends for less than 5 years.

Have the dividend payments been growing for the past 5 years? Not conclusive as the company has been paying dividends for less than 5 years.

Albertsons Companies Inc’s dividend payments are reasonably covered by its earnings and its cash flows.

Albertsons Companies Inc Valuation

Estimated intrinsic value: $54.93

Value is calculated using discounted cash flow method (taking into account their cash and debt) and scenario planning.

Projected growth rate: 4.9% - 5.8%

Beta: 0.43

Discount rate: 5.0%

Date of calculation: 14 Sept 2022

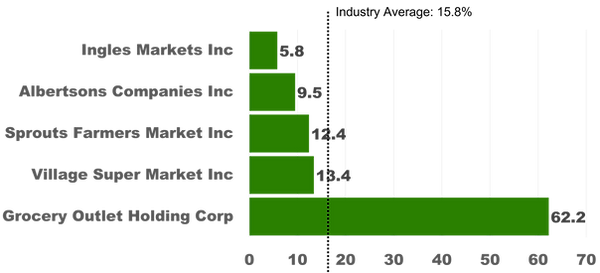

Albertsons Companies Inc Price-Earnings Ratio vs its peers

Additional Resources

I recommend reading University of Berkshire Hathaway as it greatly helps in my stock analysis. If you want a complete collection of recommended books, please visit here.

My Top Concern

Albertsons Companies Inc’s operations are dependent upon the availability of a considerable amount of energy and fuel to manufacture, store, transport and sell products. However, energy and fuel costs are influenced by domestic and international political and economic circumstances and have experienced volatility both recently and over time. Such volatility may negatively affect the results of operations.

The competition in this industry is also intense, and failure to compete successfully may adversely affect financial results.

Summary for Albertsons Companies Inc

Cost advantages and intangible assets (especially, the strength of their branding, their relationships with vendors, and the insights from customer transaction data) are generally two common economic moats in the grocery sector. With Amazon battling Walmart for national supremacy and Kroger building a highly automated fulfilment network, this intensely competitive environment requires efficiency and cost advantage to deliver returns. This is particularly true considering the sector’s low margins and limited switching costs. Unfortunately, Albertsons Companies Inc is lagging behind these.

Grocers use historical purchase data and trends to make informed decisions on their stores’ inventory and own-brand assortments, and target advertising and promotions based on customer buying history. While Albertsons Companies Inc’s loyalty program is expanding, it still lacks translating data into meaningful insights.

As a result of this discussion, I do not think that Albertsons Companies Inc possess an economic moat.

Albertsons Companies Inc’s overall performance looks decent, with revenue, net income, and operating cash flow in a growing trend over the past 5 years. Its profit margin is growing as well. The only concern is that its free cash flow went into negative territory in 2018 and 2016.

Both Albertsons Companies Inc ROE and ROIC are growing YoY over the past 5 years. Its current ROE is above its industry average of 13.7% and its current ROIC is at least 3% higher than its WACC. However, it still did not meet my minimum requirement of achieving >12% consistently. Also, I suspect that its ROE is probably skewed due to its high level of debt.

Albertsons Companies Inc’s balance sheet does not look good. Although it passes two out of four of my requirements, its net debt-to-equity ratio is high. Its net debt-to-equity is considered one of the worst in its industry. Its interest coverage is at 5.4 which is very close to my requirement of above 3.0, indicating that the financial position may change if the company does not bring in sufficient earnings.

I do not invest in no moat company. However, if you are interested in investing in Albertsons Companies Inc, you will need to have a wider margin of safety. I would suggest giving a 50% margin of safety to its estimated intrinsic value of $54.93.

Share this fundamental analysis

Please help us report any inaccurate information here. Thank you.