Altria Group Fundamental Analysis

Disclaimer: This article by The Globetrotting Investor is general in nature. We aim to bring you long-term focused analysis driven by fundamental data, hence, providing you commentary based on historical data and analyst forecasts only using an unbiased methodology. This is not a buy/ sell recommendation, and it is solely for educational purposes. Please do your research before investing. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Please read the full disclaimer here.

Altria Group

Last Updated: 27 Dec 2023

NYSE: MO

GICS Sector: Consumer Defensive

Sub-Industry: Tobacco

Share this fundamental analysis

Table of Contents

You can download a summary of Altria Group's fundamental analysis in PDF here.

Management

CEO: Billy Gifford

Tenure: 3.7 years

Altria Group, Inc.’s management team has an average tenure of 3.7 years. It is considered experienced.

Source of Revenue

Altria Group, Inc., through its subsidiaries, manufactures and sells smokeable and oral tobacco products in the United States.

Altria’s wholly-owned subsidiaries include:

-

Philip Morris USA Inc. (“PM USA”), which is engaged in the manufacture and sale of cigarettes in the United States

-

John Middleton Co. (“Middleton”), which is engaged in the manufacture and sale of machine-made large cigars and pipe tobacco and is a wholly owned subsidiary of PM USA

-

UST LLC (“UST”), which, through its wholly-owned subsidiary U.S. Smokeless Tobacco Company LLC (“USSTC”), is engaged in the manufacture and sale of moist smokeless tobacco products and snus products

-

Helix Innovations LLC (“Helix”), which operates in the United States and Canada, and Helix Innovations GmbH and its affiliates (“Helix ROW”), which operate internationally in the rest of the world, are engaged in the manufacture and sale of oral nicotine pouches.

Other wholly owned subsidiaries include Altria Group Distribution Company, which provides sales and distribution services to its domestic tobacco operating companies.

Altria's PM USA and Japan Tobacco's subsidiary, JTIUH, joined forces to create Horizon Innovations LLC (“Horizon”) in October 2022. This partnership aims to market and sell heated tobacco stick (HTS) products in the U.S. PM USA holds a 75% stake, JTIUH owns 25%, and together, they plan to expand globally.

In October 2021, UST sold its subsidiary, International Wine & Spirits Ltd. (including Ste. Michelle), in an all-cash deal worth approximately $1.2 billion, assuming certain liabilities.

Source: Altria Group

Altria Group’s reportable segments are smokeable products and oral tobacco products.

Its tobacco operating companies include PM USA, USSTC and other subsidiaries of UST, Middleton and Helix.

Cigarettes: PM USA dominates the US market with Marlboro as its leading brand, despite a 9.7% decrease in shipments (84.7 billion units) in 2022 compared to 2021.

Cigars: Middleton, known for Black & Mild, faced a 4.0% decline in cigar shipments (approximately 1.7 billion units) within the US market.

Oral tobacco products: USSTC, focusing on MST products like Copenhagen and Skoal, experienced a 2.4% decrease in shipments (800.6 million units) of oral tobacco products, including Helix's on! oral nicotine pouches. These products are primarily sold within the United States.

In December 2013, agreements were established with Philip Morris International Inc. (PMI), securing exclusive rights for the commercialization of select PMI heated tobacco products in the US. From 2019 onwards, PM USA began marketing PMI's IQOS Tobacco Heating System (IQOS System) in specific markets. These ventures, along with the financial services business and Helix ROW (Rest of World), are consolidated under an "all other" category.

Altria Group Reportable Segment Revenue FY2022

Altria Group Economic Moat

Altria Group Economic Moat

Economic Moat: Narrow

There are many ways to identify Altria Group’s economic moat, but I focus on the above 5 types. The rating is purely subjective and based on my in-depth understanding and analysis of Altria Group. Please check my summary to understand more about the economic moat.

Performance Checklist

Is Altria Group’s revenue growing YoY for the past 5 years consistently? Inconsistent.

Is the net income growing YoY for the past 5 years consistently? No.

Is the cash flow from operating activities growing YoY for the past 5 years consistently? Inconsistent.

Is the free cash flow positive for the past 5 years? Yes.

Is the gross margin % consistent/ growing for the past 5 years? Yes.

Is the EPS growing for the past 5 years? Inconsistent.

Altria Group Revenue, Net Income, Operating Cash Flow, and FCF (USD Million)

Is the free cash flow per share growing for the past 5 years? Inconsistent.

Altria Group FCF per Share

Management Effectiveness

Is Altria Group’s ROE consistently at 12%-15% YoY for the past 5 years? Inconsistent.

Altria Group's liabilities exceed its assets, so it is difficult to calculate its ROE.

Is the ROIC consistently at 12%-15% YoY for the past 5 years? Inconsistent.

Altria Group Return on Invested Capital vs Weighted Average Cost of Capital

The trendline for the number of shares outstanding is declining, which is something that an investor would be pleased to see.

Altria Group Shares Outstanding (Million Shares)

Altria Group Financial Health

Altria Group Financial Health (USD Million)

Current Ratio: 0.3 (fail my requirement of >1.0)

Debt-to-EBITDA: 2.1 (pass my requirement of <3.0)

Interest Coverage: 10.9 (pass my requirement of >3.0)

Debt Servicing Ratio: 12.1% (pass my requirement of <30.0%)

Altria Group Stock Performance

The graph below compares the cumulative total shareholder return of Altria Group’s common stock for the last five years with the cumulative total return for the same period of the S&P 500 Index and the S&P Food, Beverage and Tobacco Industry Group Total Return Index.

The graph assumes the investment of $100 in common stock and each of the indices as of the market close on 31 December 2017 and the reinvestment of all dividends quarterly.

Altria Group Stock Performance

Altria Group Intrinsic Valuation

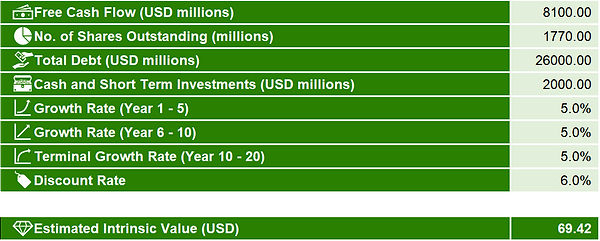

Estimated intrinsic value: USD $69.42

Value is calculated using the discounted cash flow method (taking into account their cash and debt) and scenario planning.

Average free cash flow used: USD $8,100M

Projected growth rate: 5%

Beta: 0.6

Discount rate: 6.0%

Margin of safety: 50% (Uncertainty: High)

Price range after the margin of safety: <$35.00

Date of calculation: 27 Dec 2023

Altria Group Valuation

Free cash flow used is a weighted average that is rounded to the nearest tens. In some instances, I used a more realistic number to represent the free cash flow.

Total debt and cash and short-term investments are last quarter figures that are rounded to the nearest tens. In some instances, I used more realistic numbers to represent them.

Altria Group Intrinsic Valuation

Altria Group Relative Valuation

Altria Group Price-Earnings Ratio vs its peers

Altria Group Historical Price-Earnings Ratio

Additional Resources

I recommend reading The Five Rules for Successful Stock Investing as it greatly helps in my stock analysis. If you want a complete collection of recommended books, please visit here.

My Top Concern

One of the key concerns that I have when investing in tobacco companies is the unfavourable litigation outcomes that could affect the business.

Altria and its subsidiaries, including PM USA, can face legal proceedings in the U.S. and foreign jurisdictions on a variety of claims such as product liability, unfair trade practices, antitrust, tax, patent infringement, RICO violations, and employment matters.

Legislative action may also expand the types of claims and remedies available to plaintiffs. It could also encourage the beginning of additional litigation.

While Altria Group has achieved substantial success in managing litigation, there remain considerable challenges. An adverse outcome or settlement of certain pending litigation could still materially affect their financial position.

Next, Altria Group is dealing with significant governmental and private sector actions aimed at reducing tobacco use and holding the company responsible for the health effects associated with smoking and exposure to environmental tobacco smoke.

These actions, together with the declining social acceptance of smoking, have resulted in reduced cigarette industry volume, and we expect this trend to continue.

Moreover, actions by the FDA and other governments or agencies could impact adult tobacco consumer acceptability of or access to tobacco products.

These actions could restrict adult tobacco consumer choices, limit the launch of new or modified tobacco, impose additional manufacturing, labelling or packing requirements, or even restrict the use of specified tobacco products in certain locations. These actions can undermine Altria’s business.

Lastly, Altria faces fierce competition in the tobacco market, which includes factors such as quality, taste, price, innovation, marketing, packaging, and distribution.

The growth of new product categories, such as e-vapour and oral nicotine pouches, has contributed to a decrease in cigarette consumption and sales. Unregulated synthetic nicotine products could also negatively impact growth. All this competition can harm Altria's profitability and market share.

Summary for Altria Group

Altria Group’s economic moat stems from its intangible assets which in turn help establish a high barrier to entry.

The intangible assets of the company, and its subsidiaries, come from the addictiveness of its products, and the tight industry regulation.

The presence of nicotine in tobacco makes it an addictive substance and this suppresses the cessation rate. Research has shown that most smokers who attempt to quit fail to do so.

Additional research suggests that premium price segments are associated with lower cessation rates. With around 90% of Altria cigarette volumes from premium categories, the company has a stronger foothold in the premium segments than its competitors.

The company’s strong intangible assets also come from the tight government regulations in the tobacco industry. The tight government regulations in the tobacco industry limit market share volatility and competition on price.

The FDA's restrictions on marketing new or modified products make it difficult for new entrants to launch new products, and even if they receive FDA approval, regulations on tobacco advertising severely restrict their ability to gain the attention of smokers.

These regulations have resulted in a lack of marketing communication and have discouraged consumers from switching brands, helping Altria Group to maintain its sales volume.

Strong brand equity also plays a part in reinforcing Altria Group’s intangible assets.

Despite eroding brand loyalty in other consumer product categories, brand equity remains relevant in tobacco. Altria Group's Marlboro brand is a dominant player in the premium price segment, which is associated with higher brand loyalty.

However, there are many other areas of the economic moat that Altria Group is lacking. Hence, I will only give the company a narrow economic moat rating.

Altria Group's performance over the past five years reflects a mixed picture. While the revenue trajectory has not been showing a clear trend of year-on-year growth, the company has maintained a positive free cash flow throughout this period.

Similarly, the gross margin percentage has remained consistent, indicating stability in this aspect. However, the net income, cash flow from operating activities, EPS, and free cash flow per share have shown inconsistency in their growth patterns over the same timeframe.

Altria Group's capital management strategy showcases a mix of trends over the past five years. The ROE and ROIC have shown inconsistency, fluctuating above and below the 12%-15% range annually.

Due to liabilities surpassing assets, calculating ROE becomes challenging. However, the company maintains an ROIC higher than its WACC, indicating efficient use of invested capital. Notably, Altria Group has been steadily reducing its number of outstanding shares, a positive move for investors as it can enhance earnings per share over time.

The company’s financial health presents a mixed scenario based on key metrics. The current ratio, at 0.3, falls below the preferred threshold of 1.0, indicating potential difficulty in meeting short-term obligations with current assets. However, the debt-to-EBITDA ratio stands at a favorable 2.1, signifying a manageable level of debt concerning earnings.

Additionally, the interest coverage ratio suggests the company's ability to cover interest expenses. Moreover, the debt servicing ratio indicates that Altria Group dedicates a modest portion of its income towards servicing debt obligations, portraying a healthy financial position in terms of debt management despite challenges reflected in the current ratio.

Investing in Altria Group demands caution due to several factors. The company exhibits a narrow economic moat, indicating limited competitive advantages that may affect its long-term sustainability. Its performance and capital allocation haven't been satisfactory, coupled with an unstable balance sheet that raises concerns about financial stability.

To consider an investment, a high margin of safety of at least 50% is essential, allowing for a significant buffer against potential risks and uncertainties inherent in the company's operations and financial situation.

Share this fundamental analysis

Please help us report any inaccurate information here. Thank you.